🚨Letitia James’ FRAUD SCANDAL Just BLEW UP as 42 YEARS of Alleged FRAUD Under Investigation | HO~

New York Attorney General Letitia James is facing a crescendo of scrutiny as fresh allegations and online claims suggest that the legal saga surrounding her personal real estate history could be far from over. What began as a narrow focus on a single Virginia property has, in recent days, widened into a sprawling narrative: that prosecutors may examine multiple properties and a decades-long paper trail.

While the facts remain contested and much of the conversation is fueled by outside commentators, the political and legal stakes are unmistakably high.

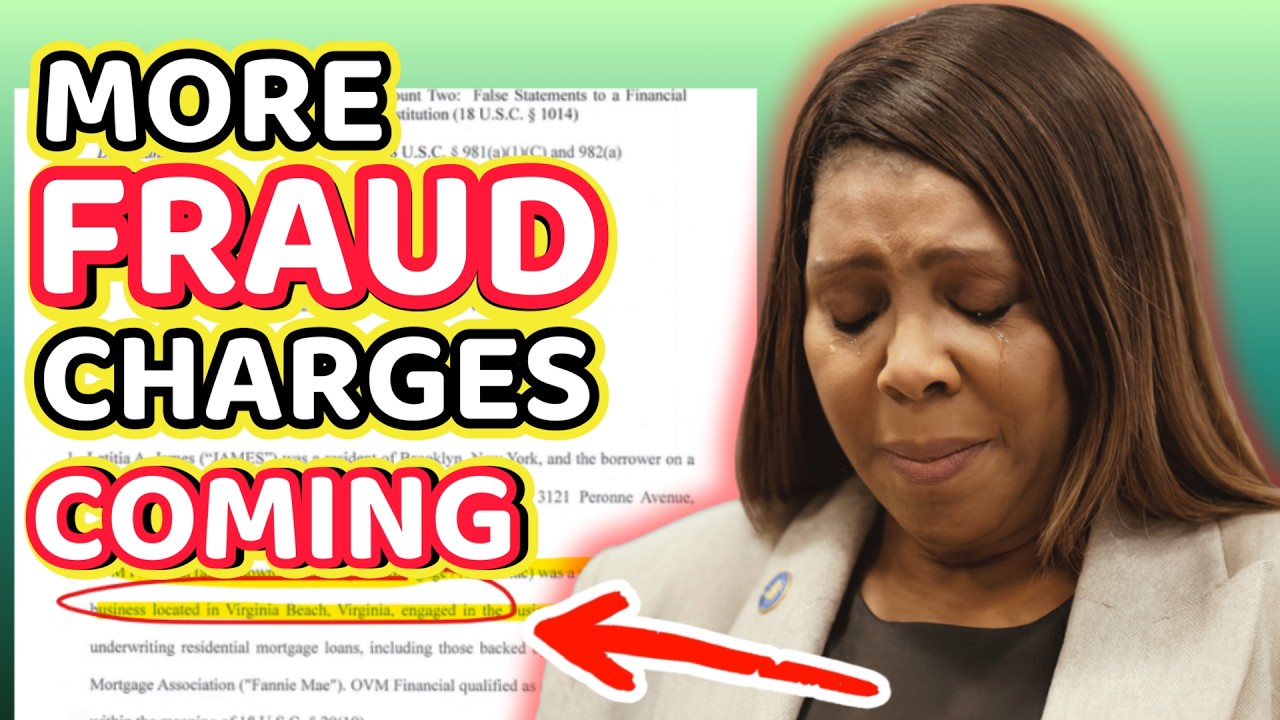

At the center of the furor is a straightforward but explosive theory that has captivated commentators: that James presented one set of facts to lenders and another to tax authorities.

The heart of the claim is familiar to anyone who has followed mortgage enforcement cases: a property categorized as a “second home” to secure favorable loan terms, while reportedly appearing as an income-generating asset on tax filings—potentially qualifying for deductions and different financial treatment.

It’s a clean narrative that advocates say a jury could easily understand: what was said on loan documents, what was claimed on tax returns, and whether discrepancies, if proven, were intentional and material.

But the newest twist isn’t about a single mortgage. It’s the assertion, promoted by a forensic accounting commentator who says he began reviewing James’s public disclosures months ago, that irregularities could extend far beyond one address.

In on-air interviews and social media posts, he has alleged that the pattern stretches across three properties and, more dramatically, across 42 years of mortgage paperwork—claims he argues are consistent with a “modus operandi,” not an isolated oversight. Those allegations, unproven as of now, have nevertheless energized critics and set off a wave of speculation about whether prosecutors could seek to introduce evidence of a broader pattern to support intent.

The legal mechanics of such a move would be complex. In federal practice, prosecutors sometimes use “pattern evidence” under rules that allow limited introduction of other acts to prove intent, knowledge, or absence of mistake.

Defense counsel typically push back hard, arguing that these historical episodes are prejudicial, unrelated, or insufficiently similar to be relevant. Judges must weigh probative value against unfair prejudice, often trimming back the scope of what a jury can see. If this case reaches that stage, the admissibility of decades-old documents could become a critical battleground.

Equally consequential are the claims surrounding insurance. Analysts note that occupancy status—primary residence, second home, or rental—doesn’t just affect loan pricing; it also drives how insurers underwrite risk, set premiums, and draft policy terms. If an owner represents a property as owner-occupied to obtain lower premiums while treating it as a rental for tax purposes, insurers could view that as material misrepresentation.

Whether such facts exist here, and whether they would rise to criminal exposure rather than a contractual dispute, would depend on documents, timelines, and intent—details that remain out of public view.

One element fueling the public’s fascination is the notion that the case is “simple.” Mortgage and insurance cases often drown in technicalities, but the story being told by outside commentators is notably linear: signed forms, explicit boxes ticked, and statements that can be directly compared across systems—banks, tax returns, and insurance applications. That clarity, if it survives legal vetting, could be potent.

Yet defense attorneys warn that simplicity can be misleading. Borrowers often rely on third-party professionals, and occupancy status can change legitimately after closing. A common defense in such cases is that a property was initially acquired as a second home and later converted to a rental—an explanation that forces prosecutors to show the original intent was false at the time of loan origination.

The noise surrounding James’s Brooklyn property adds a separate, technical layer. Critics argue that the building’s unit count, as reflected in official certificates of occupancy, should have driven different financing and insurance classifications.

If a building is five units rather than four, it can shift from residential into commercial frameworks, affecting loan terms, disclosure obligations, and coverage types. Here again, context matters: changes in configuration, legacy paperwork, and agency approvals can create gaps that aren’t necessarily criminal. Untangling those facts will be central to any prosecutorial decision-making.

Even as these allegations proliferate, procedural realities loom. Any case would have to withstand motions to dismiss, where defense attorneys argue that charges fail as a matter of law or lack sufficient factual grounding.

Should the matter proceed, discovery would bring detailed exchanges of documents and witness statements, exposing whether online claims align with bank files, tax submissions, title records, and insurance policies. The results could affirm suspicions—or undercut them.

Politics, meanwhile, shadows every development. James has been a high-profile figure in politically charged litigation, making her a lightning rod for partisan narratives. Allies portray the allegations as retaliatory, emphasizing the presumption of innocence and the risk of normalizing criminal probes based on public speculation.

Critics contend that accountability must apply evenly, particularly to officials entrusted with enforcing financial laws. That divide ensures any step—from motions practice to potential trial—will be read through a political lens, complicating the task of a judge seeking a fair jury.

For the broader public, the case touches on foundational questions about transparency and trust. How should institutions handle allegations that cut close to their own credibility? When does secrecy protect due process, and when does it breed suspicion?

Observers recall prior episodes in financial enforcement where the perception of double standards—one set of rules for the powerful, another for everyone else—left lasting scars. Those scars are part of why a story about line items on mortgage forms can command outsized attention.

There is also a cautionary dimension: the digital information cycle can outpace legal verification. Claims spread fast; corrections rarely catch up. Responsible disclosure, if it comes, would likely be incremental—court filings, hearing transcripts, and selective exhibits—rather than a wholesale release.

While that pace frustrates audiences conditioned by viral timelines, it’s how courts preserve accuracy and protect the rights of victims, witnesses, and uncharged third parties.

If the matter advances, expect several key inflection points:

Motions to dismiss: a legal stress test for the sufficiency of charges.

Discovery disputes: fights over access to tax records, lender files, underwriting narratives, and insurance applications.

Rule 404(b)-style arguments: whether alleged prior irregularities are admissible to show intent or pattern.

Expert testimony: dueling experts on mortgage underwriting, occupancy standards, insurance risk, and materiality.

Jury selection: a high-stakes process in a politically saturated environment, where pretrial publicity and partisan identity could shape voir dire.

Potential outcomes span a wide spectrum. The case could be narrowed significantly by pretrial rulings; it could resolve with a negotiated agreement; or it could proceed to trial on a streamlined theory, focusing on the clearest documentary contradictions.

Sentencing exposure in white-collar matters often turns on loss calculations and intent, but reputational consequences can be decisive regardless of criminal penalties. For an elected law enforcement official, even an unresolved cloud can be career-altering.

For now, what is certain is the intensity of public interest. The narrative—one of alleged discrepancies between what was told to banks, claimed to tax authorities, and conveyed to insurers—offers a rare window into the interconnectedness of financial systems. A single unchecked box can cascade across mortgages, policies, and returns, amplifying consequences.

That’s why, in the court of public opinion, the story feels larger than one person: it is a referendum on whether paperwork precision is an equal-opportunity obligation.

Supporters of full accountability urge patience and rigor. They argue that if evidence exists, it should be tested in court, not litigated primarily through commentary clips and social media threads. Critics of the process warn that delay can look like denial, and that a painstaking legal cadence risks losing public confidence. Both concerns are valid—and in tension.

As the debate continues, one principle should be non-negotiable: claims this significant deserve verification by documentary evidence and judicial oversight. Allegations about 42 years of conduct, three properties, and overlapping insurance and tax issues can’t be resolved by rhetoric alone. They require records, testimony, and rulings that meet the standard of law, not just the tempo of the news cycle.

If clarity comes, it will likely arrive in pieces—through filings, hearings, and reasoned opinions that separate procedural noise from probative fact. Whether that clarity vindicates, implicates, or lands somewhere in between, it will test not only the subject of the allegations but also the public’s capacity to absorb a complex truth without forcing it into a simple narrative.

Editor’s note: This article is a simulated, news-style reconstruction based on an unverified outline provided by a reader. It does not assert that any indictment or investigation described herein has occurred. Readers should consult primary court records and reputable outlets for verified updates.

News

A wealthy doctor laughed at a nurse’s $80K salary backstage. She stayed quiet—until Steve Harvey stepped in and asked. The room went silent. Then Sarah cried—not from shame, but relief. Respect isn’t a title. | HO

Chicago Memorial chose two families from the same institution for a special episode—healthcare workers on national TV, the pitch said,…

On Family Feud, the question was simple: ”What makes you feel appreciated?” She buzzed in first—then her husband literally stepped in front of her to answer. The room went quiet. Steve didn’t joke it off; he stopped the game. The real surprise? Her honest answer finally hit the board. | HO

Steve worked the crowd like he always did. “All right, all right, all right,” he called, voice rolling through the…

He didn’t walk into the mall looking for trouble—just a birthday gift. When chaos hit, he disarmed the shooter and held him down until police arrived. Witnesses begged the officer to listen. Instead, the ”hero” was cuffed… and the cop learned too late | HO

He stayed low, using shelves as cover, closing distance step by silent step. For him, this was a familiar equation:…

Three days after her dream wedding, she learned the unthinkable: her ”husband” already had a wife. | HO

Their marriage didn’t look like the movies. It looked like overtime and budgeting apps and Zoe carrying the weight of…

Steve Harvey STOPPED Family Feud Mid-Taping When Celebrity Did THIS — 50 Million People Watched | HO!!!!

During a short break in gameplay while the board reset, Tiffany decided to “work the crowd,” something celebrity guests often…

She Allowed Her Mother To ‘ROT’ On The Chair And Went To Las Vegas To Party For 2 Weeks | HO!!!!

Veretta raised Kalin with intention: discipline mixed with tenderness. Homemade lunches in brown paper bags. Sunday mornings at Greater Hope…

End of content

No more pages to load